The Present and Future of FX Execution Algorithms

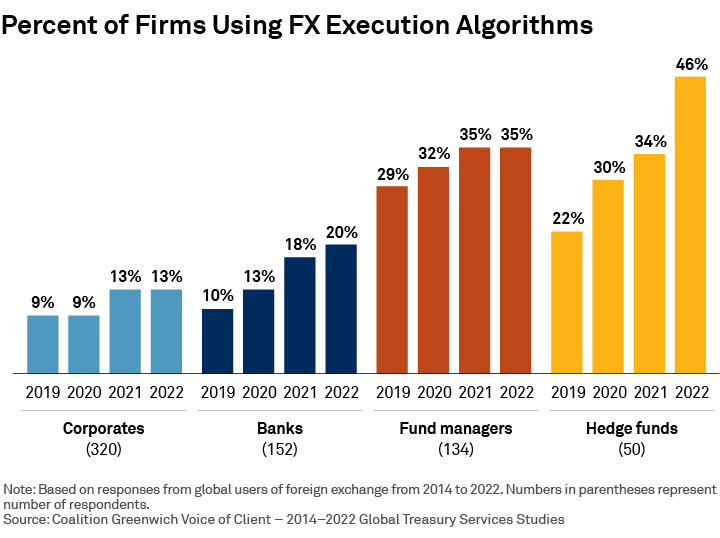

After years of mediocre growth, FX execution algorithm adoption is looking up. Most buy-side segments have witnessed a healthy rise in the use of algos since 2020, especially on the real money side. Both fund managers and hedge funds have seen an uptick of algo use, with adoption now at 30% and 40%, respectively.

Growth in algo adoption is a solution to a long-lived problem. The buy side is increasingly dealing with fragmented liquidity and a need to execute transactions more efficiently. By using FX algos, the buy side benefits from improved technology designed to address gaps in liquidity, data and other inefficiencies tied to over-the-counter markets.

The FX Global Code (FXGC) emphasizes transparency. It turns out, improved technology and greater efficiencies on the desk are not the only drivers of algo adaption. Principle 18 of the FXGC includes guidance for algo providers, shining a light on how algos are marketed and managed. The FXGC emphasizes transparency and disclosure requirements that are intended to help consumers of algos understand more thoroughly the nature of the tools they may (or may not) use. It appears the more the industry knows about a product, the more likely they are to use and trust it.

Has the adoption of FX algos plateaued? Because FX algo use has not achieved the same market share as in other asset classes, it is fair to ask if adoption is leveling off. Our data shows the answer is a resounding “no.” Trading in size in difficult markets require finesse and creativity, which algos can provide.

Of course, creativity also comes into play when deciding which algo is most suited for the market conditions in which participants are trying to execute. This often requires sell-side guidance to help buy-side traders use the optimal tool for the market conditions. (Spoiler alert: Despite the popularity of algos, relationships still matter.) In equity markets, these challenges spawned “algo wheels”—something likely coming to FX markets.

Where will more algo adoption take place going forward? The opportunity for additional algo growth sits squarely in other FX products. The value of algorithmic execution in FX spot is mostly understood, and adoption will continue to rise. The ability of algo providers to apply this technology to other instruments such as non-deliverable forwards (NDF) represents an area of potential usage. To date, uptake has been limited.

Talk of the use of algos in certain FX swaps and options—particularly non-standard dates—is probably sometime away. However, if the trajectory of electronic trading and algo use gleaned from other asset classes is any indicator of the future of FX algo adoption, the prospects of broad adoption are very good.