Transparency is Coming for Portfolio Trading

Table of Contents

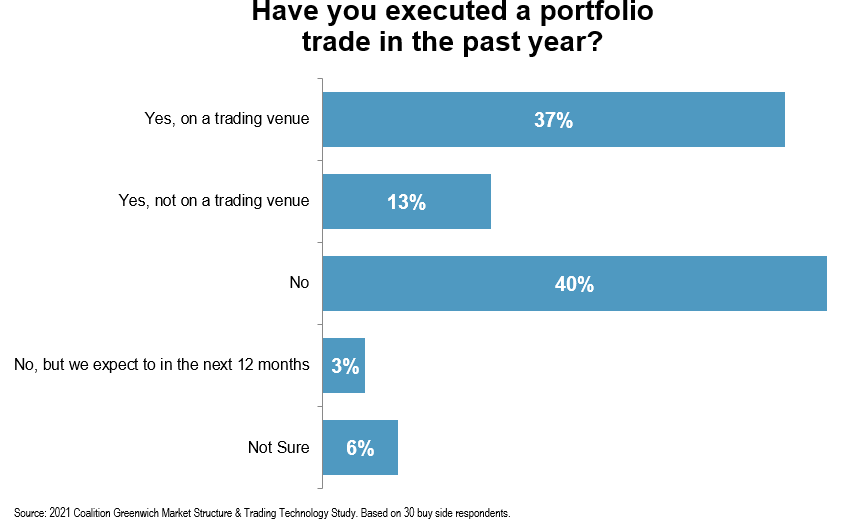

The days of corporate bond portfolio trading estimates are coming to an end. FINRA has proposed and the SEC has approved a new rule (proposed FINRA Rule 6730(d)(4)(H)) that will require corporate bonds traded via a portfolio trade be reported to TRACE with a "designated modifier"—or put more simply, a portfolio trading flag. The new rule comes about two years after the SEC's Fixed Income Market Structure Advisory Committee (FIMSAC) recommended the change and grows in importance with half of the 30 buy-side firms Coalition Greenwich spoke to in Q4 2022 having executed a portfolio trade in the past 12 months.

A New Reporting Flag

While the new reporting flag will help market participants and analysts like us gain deeper insight into the size of the corporate bond portfolio trading market (which, for the record, is roughly 5% of the total market, depending on the month), the true purpose of the change is to provide improved post-trade price transparency to the market as a whole. Here is how the proposal explains it (emphasis ours):

FINRA rules do not allow for reporting of a single portfolio trade with an aggregated price. Instead, a member firm must report to TRACE a trade for each individual bond in the portfolio with an attributed dollar price for each bond. FINRA believes that, in many cases, the reported price for each bond in a portfolio trade is in line with the bond’s current market price, while in other cases the attributed price reported for an individual bond might deviate from its current market price.

Basically, bonds traded on their own can often trade at prices different than the same bond traded as part of portfolio. It’s not that this shouldn't happen but, instead, that the market needs to know the price reported was a "portfolio price," so they understand why their dealer might quote them a different price when trying to buy or sell the same bond.

Portfolio trades must be reported with the new flag when they meet the following criteria:

i) is executed between only two parties

(ii) involves a basket of corporate bonds of at least ten unique issue

(iii) has a single agreed price for the entire basket

This is largely in line with the industry's view and matches our definition per the research we published examining the benefits of portfolio trading in 2021.

Industry Support for Transparency

This new rule is also one of the few that is coming to market with few if any dissenters. The fact that only three comment letters were submitted—most of which were positive—demonstrates the industry's support for this new level of transparency.

FINRA has about three months to define exactly how the flag will work in practice, and then another year within which to implement the rule. A go-live in 2023 seems the most likely outcome. Until then, we expect that the race to capture portfolio trading activity by the trading venues will continue in earnest, while corporate bond dealers focus on improving their ability to quote portfolio trade prices quickly as buy-side demand continues to grow.