FTX Collapse Points to Need for Greater Adoption of Institutional-Grade Custody, Regulation

Table of Contents

For the past few years, a large percentage of the digital asset community has gravitated to vertically integrated platforms to trade, settle, custody, and lend/borrow digital assets. Vertically integrated business models have been a convenient way to offer services to investors in a single package, including investing, trading and participation in yield activities.

Notable examples of vertically integrated business models in the U.S. include Coinbase and FTX.US, which both combine retail-focused trading with institutional capital markets activities.

Even before the collapse, FTX.US was an interesting example. It functioned as a broker-dealer, swap execution facility (SEF), Derivatives Clearing Organization (DCO), Designated Contract Market (DCM), and also had U.S. state money transmitter licensing. All that allowed it to offer both “spot” crypto and derivatives on the same platform.

Much has been made of FTX’s desire to acquire all the necessary licenses via acquisitions (i.e., via LedgerX) or on their own, including their minority investment in IEX, to support regulatory hedging and overall strategy.

But now, the FTX collapse has turned that model on its head. It is remarkable how swiftly FTX collapsed, and the implications will takes months to reverberate around the industry. Memories will be long. The list of institutions invested in FTX is extensive and includes some of the most well-known names in venture investing and private equity. The institutional community will take a hit, and it will take time to for investors to settle and recommit to crypto.

Separation of Trading and Custody

While the FTX situation remains opaque and quickly evolving, we can already point to changes to come. The inability for investors to recover their digital assets drives home the importance of digital asset custody models and relationships. The collapse of a broker-dealer should simply not impact the ability of clients to recover their assets in custody.

At FTX, apparently the assets were not in verifiable, segregated accounts held on-chain, with the movement of the assets controlled by the asset owner. These assets were likely held in omnibus accounts managed by FTX and comingled with the assets of other business entities. This comingling reached epic proportions, according to press reports. Moreover, the assets do not appear to be bankruptcy remote.

Because this collapse affects not only FTX’s own investors, but also the ability for FTX clients to recover their assets, we believe defining institutional-grade custody and best practices will be moved up the priority list in the coming weeks and months.

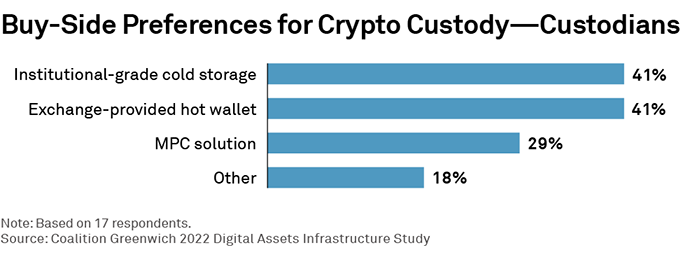

Our research shows that institutional-grade cold storage and exchange wallets were neck and neck in popularity among professional investors as of a few weeks ago. The FTX collapse puts the exchange-based custody model under extreme scrutiny. The counterparty risk was always known and accepted, but full-scale bankruptcies always seemed somehow out of scope. No more.

As firms consider the available range of hardware- and software-based storage options, such as cold storage and multi-party computation (MPC), institutional-grade solutions are likely to become far more popular and crowd out the exchange-provided wallets (by demand and later by regulatory edict.)

Government Action

Also moved up on the priority list: regulatory oversight. There will clearly be hearings on the FTX matter, and Congress will (try to) act. After a brief pause while the market settles down and digests, we expect the following:

- Existing bills already before Congress will be modified or scrapped altogether.

- U.S. regulators will move swiftly. Both the CFTC and SEC can move without agreeing fully on how to define these digital assets (securities vs. commodities) under existing rules.

- U.S. regulators will seek to separate proprietary trading activities from any U.S. crypto platform that seeks to define itself as a regulated exchange or alternative trading system (ATS).

- U.S. regulators will likely require that custody be separated from other exchange activities.

- The SEC will move to further define a “qualified custodian” or QC for digital assets. (According to our research, almost two-thirds of buy-side firms report they do not fully understand rules defining what it means for their custodian to be a qualified custodian (QC) for digital assets.)

- Institutional-grade custodians, particularly those with well-established brands, secure technology and healthy balance sheets, will see their solutions more heavily sought after (with their segregated accounts on-chain, insurance, bankruptcy remoteness, KYC/AML, etc.).

Institutional activity was really only just beginning when the FTX collapse occurred. Adding clarity on custody, in particular, could go a long way to further continuing the floodgates of institutional flows into digital assets, once the FTX dust starts to settle and the industry is ready to move forward. Despite the volatility, even Man Group Plc is reported to be close to launching a crypto hedge fund this week.

Ultimately, digital asset custody is a matter of trust. Bankruptcy remoteness, or the lack of it, is a concern that we have heard come up time and time again from institutional investors, even before this most recent mess. Now investors are being forced to face the worst-case scenario.

Bringing more institutions into digital assets will (now more than ever) require the continued build-out of a robust technological and operational infrastructure to support trading and investing. Moreover, regulatory clarity, along with education by custodians about different custody options, will help firms better integrate digital assets into their investment frameworks, while reducing the tail risk that we’ve now come to know is very real.